CMDI proposals could prompt downgrades, MREL supply, but tough discussions ahead

A slew of downgrades could result from the latest EC proposals to reform the EU resolution framework, while smaller and medium-sized banks could approach the capital markets for MREL issuance. However, with national interests and supportive regulators set to clash over the proposals, the final shape of any changes is unclear. Neil Day reports, with insights from Crédit Agricole CIB and Moody’s.

You can download a pdf of this article by clicking here.

Photo: Commissioners Mairead McGuinness and Valdis Dombrovskis, and spokesperson Sonya Gospodinova announcing the proposals; Credit: Valentine Zeler/EC

European Commission proposals to position all depositors above senior unsecured debt in banks’ liability hierarchies could trigger Moody’s downgrades of many banks’ bonds and prompt shifts in funding strategies, although the initiative is already encountering resistance.

Released on 18 April, the crisis management and deposit insurance (CMDI) framework proposals have been under discussion for several years, but found renewed resonance in the wake of the collapse of Silicon Valley Bank (SVB) and emergency rescue of Credit Suisse in March.

As well as aiming to increase confidence in the banking sector and reduce the chances of a bank run, the measures seek to reduce the likelihood of taxpayer money being used to support banks outside the EU resolution framework, and make it easier and more likely for deposit guarantee schemes and resolution funds to be used instead and as envisaged according to previous initiatives such as the BRRD.

“Today we are taking another step forward to ensure all failing banks can be handled more effectively and coherently should the need arise,” said Valdis Dombrovskis, Commission executive vice president for an Economy that Works for People. “Our principles remain the same: to preserve financial stability, protect taxpayers’ money and improve depositor confidence.

“These proposals will also help to finalise the Banking Union: a cornerstone of a successful Economic and Monetary Union.”

The core part of the CMDI package consists of three legislative proposals making targeted amendments to the BRRD (Bank Recovery & Resolution Directive), the Single Resolution Mechanism Regulation (SRMR), and the Deposit Guarantee Schemes Directive (DGSD).

While the ambition of expanding resolution to encompass more small and medium-sized banks — as opposed to liquidation under national insolvency proceedings — had been expected, the proposed introduction of general depositor preference was less anticipated. A goal of the latter, as well as the proposed pari passu ranking of all deposits, is to help make possible the financing of resolution measures by funds in deposit guarantee schemes (DGS).

Instead of enjoying a super-senior ranking, insured deposits and hence DGSs will rank pari passu with non-insured retail deposits and uninsured institutional depositors, increasing their ability to absorb losses, in parallel with an increase in the cost of compensating depositors, and potentially contributing to the 8% TLOF criteria required to access resolution funds.

“The overall result is that DGS would be able to absorb losses at an earlier stage, giving governments a greater incentive to deploy resolution tools rather than wait for the bank to be liquidated,” noted Moody’s. “DGS could if necessary provide the resources needed to protect the depositors of smaller banks in resolution after their bondholders had been bailed in. The relevant national resolution fund (or SRF (Single Resolution Fund) in the case of the Single Resolution Mechanism) would compensate the DGS if the cost of its intervention in resolution turned out to exceed the cost of a liquidation.”

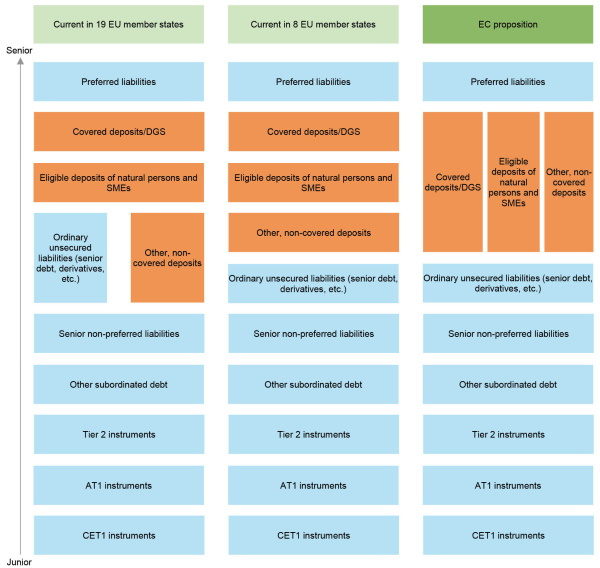

Current and proposed EU bank liability hierarchy

Source: European Commission, Moody’s

From ‘de facto’ to ‘de jure’

As alluded to by the rating agency, under the Commission’s proposals, all depositors across the EU would rank higher than senior unsecured bondholders. While this is in line with the prevailing hierarchy in eight EU member states (including Italy and Portugal, for example), it will represent a significant change in the majority, including jurisdictions such as France, Germany and Spain.

“The EC’s proposal for full depositor preference is credit negative for senior unsecured debtholders in these jurisdictions, since their claims would no longer benefit from loss-sharing with depositors,” said Moody’s.

“Conversely, there would be an additional benefit for uninsured institutional deposits. These would now not only hold equal rank with all other deposits — as in the case of the seven current full depositor preference countries — but they would also benefit from greater volumes of subordinated liabilities, now including senior unsecured debt, to absorb the burden of losses before depositors.”

While Fitch and S&P do not anticipate the proposed general depositor preference to result in rating actions, Moody’s has highlighted the potentially widespread impact that would ensue under its methodology for banks in jurisdictions facing change.

Although Moody’s in its credit opinions of banks places most weight on the current legal liability EU pari passu waterfall — dubbed the “de jure” waterfall — it also bears in mind the discretion resolution authorities have when applying resolution measures. It captures this possibility that depositors may ultimately be ranked above senior unsecured bondholders — the “de facto” waterfall — by assigning this scenario a 25% weighting versus 75% for the de jure scenario.

“The de jure scenario of tomorrow is more or less the de facto scenario that we already run and which is reflected in our credit opinions,” explains Alain Laurin, associate managing director, EMEA banking, at Moody’s.

Under the rating agency’s Advanced LGF analysis, whereby notching for different liability classes is based on their assessed loss severity, divergence between deposits and senior unsecured ratings could occur more often if the CMDI proposals are implemented in their current form.

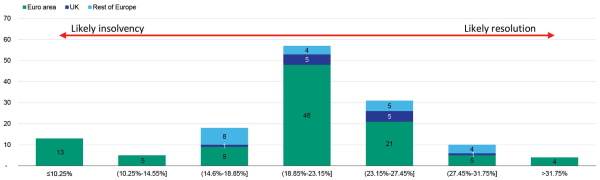

In response to strong interest from investors, Moody’s at the end of May published an analysis of the potential impact of the proposals on 119 banks that have relevant public information available. This found that deposit ratings would enjoy higher notching uplift for 47, and that senior unsecured debt notching would be lower for 89. The rating agency’s data shows that at least a dozen senior unsecured ratings could fall out of both the double-A and single-A categories, while a couple could be downgraded to junk, all other things being equal — not a given at this early stage.

Moody’s distribution of current senior unsecured or issuer ratings in EEA countries by rating and difference under the full depositor preference (“de facto”) scenario

Scorecard data is as of 26/5/23. Excluded are those ratings based on private LGF data and where current assigned LGF notching differs from the weighted outcome of the de jure and de facto scenarios. Rating categories with no entries omitted. Source: Moody’s

A Crédit Agricole CIB analysis painted a similar picture, finding that around 90% of larger banks’ senior preferred ratings are at risk of being downgraded by one notch, while 50% of deposit ratings could see a one-notch upgrade.

“Clearly there could be some impact on funding costs from a rating downgrade,” says Alpesh Varsani executive director, DCM financial institutions, at Crédit Agricole CIB. “It’s difficult to put a number on that, but where key rating thresholds are crossed, we would expect a more material impact on investability and pricing, as well as where they sit in the various indices.”

Such a scenario would also see the notching and hence pricing differential between senior preferred and senior non-preferred debt narrowing. This could mean that, although larger banks’ funding and capital requirements will not change as a result of the proposals, they explore ways of tamping down their costs.

“It’s very early days,” says Varsani, “but if banks just need funding and don’t need to issue for MREL, they could potentially in future do this not via senior unsecured debt but via a new form of instrument, a structured deposit, that could benefit from being higher up in the hierarchy and so cheaper than where senior preferred is today.”

Changes to spur MREL issuance

The CMDI proposals could meanwhile see more small and medium-sized banks facing MREL requirements, a pre-condition of accessing resolution funds, given the Commission’s goal of resolution being preferred to liquidation or other solutions outside the EU resolution framework.

For instance, Moody’s notes that a key objective of the package is to allow DGS to play a role in facilitating “purchase and assumption”, whereby the assets and liabilities of a failed bank are acquired by a functioning peer, for mid-sized European lenders.

“Their contribution would be capped at their exposure in an insolvency, and would not exceed any shortfall in the value of assets transferred to match the deposits and more senior liabilities assumed by the acquirer,” said the rating agency. “DGS funding would also be conditional on the failed bank holding proportionate volume of MREL to facilitate a transfer strategy.

“This would likely result in a much larger number of EU banks being required to hold an RCA (recapitalisation amount) as part of their overall MREL requirement.”

A host of smaller and medium-sized banks could therefore enter the public senior debt market in the future, says Varsani (pictured).

However, Laurin sees two categories of banks: those subject to a positive recapitalisation amount; and those that are only required to comply with the loss absorption amount (LAA) (the RCA being set at zero).

Furthermore, he notes the oft-cited mantra of Single Resolution Board (SRB) officials, that when it comes to resolution in line with the BRRD, “it is for the few, not the many”. According to Moody’s, while the SRB is the resolution authority to 120 of the largest European lenders, the size of current RCA requirements for the remaining 2,085 euro-area institutions suggests just 64 would be resolved.

“The problem for these retail banks is that they collect deposits, do not need funding, and they cannot easily access the capital markets,” adds Laurin. “So issuing to meet MREL requirements will not be straightforward.

“So perhaps MREL requirements will be imposed for only a very few of the mainly larger medium-sized banks.”

MREL requirements in Europe (% of Total Risk Exposure Amount (TREA))

Source: Company reports, Moody’s

ECB supportive, but battles ahead

A lengthy and difficult legislative process is anticipated, until at least 2025, and some question whether the CMDI proposals will ultimately be implemented. This is partly because they are seen as another step on the road to the envisaged European Deposit Insurance Scheme (EDIS), which has been on the backburner for some time due to political hurdles that the latest initiative only underline.

“The larger banks in the larger countries such as France and Germany already represent the biggest contributors to the SRF as well as their national DGS,” says Varsani, “and having an expanded scope could mean they are expected to contribute more in order to support smaller banks — and the objections are only going to be stronger if it’s now on a Europe-wide basis.”

A consultation is underway until at least 29 August (after having been extended to allow for EU translations), but the first feedback has already been submitted and published on the Commission website, and the German Savings Banks Association (DSGV) has objected to the proposals. Market participants had anticipated resistance from Germany — partly due to how the measures could clash with national institutional protection schemes (IPSs) — and the association objects to several key elements of the proposals.

The DSGV echoes Laurin’s comments on the difficulty of smaller banks issuing debt to meet MREL requirements, as well as DGS contributions in the context of resolution.

“The proposed approach of making resolution the standard for crisis management in the banking sector,” it says, “is foreseeably more bureaucratic and financially burdensome, especially in the case of small and medium-sized institutions.”

As well as the two responses included on the Commission consultation website as of Friday (14 July), the European Central Bank on 5 July published an opinion on the proposals, after the SRB and ECB had initially published a joint statement welcoming them on the day they were released.

The central bank welcomed the proposed expansion of resolution for smaller and medium-sized credit institutions, adding that it is imperative that this be accompanied by adequate resolution funding.

“Without improved access to funding, expanding the scope of resolution risks being impossible to implement in practice,” it said. “The ECB therefore fully supports that, building on the principle that losses in a credit institution failure should be borne first and foremost by shareholders and creditors, the proposed legislative package also provides for a stronger role for deposit guarantee schemes in resolution, subject to certain safeguards.

“It is important that such role is facilitated by a harmonised least-cost test and a single-tier depositor preference.”

Among other elements of its feedback, the ECB proposes to give IPSs preferential treatment, and also seeks to ensure that there are adequate safeguards for accessing resolution financing arrangements in cases of systemic crises.