Return towards IG: Today’s FIG landscape a promising stage for next Greek adventures

Buoyed by the return to investment grade of the Hellenic Republic, Greek issuers have been given an increasingly warm welcome by investors across asset classes. In Athens on 29 February, Crédit Agricole CIB syndicate, DCM, advisory and research set the scene for Greek banks’ next steps as they navigate the maze of risks and opportunities in today’s FIG market.

You can download a pdf version of this article here.

Panellists (below, left to right):Michael Benyaya, co-head of DCM solutions and advisory, Crédit Agricole CIB

Bert Lourenco, global head of rates research, Crédit Agricole CIB

Yves Glaser, head of financial institutions advisory, EMEA, Crédit Agricole CIB

Vincent Hoarau, head of FIG syndicate, Crédit Agricole CIB

Michael Benyaya, co-head of DCM solutions and advisory, Crédit Agricole CIB: To set the scene, what is the central scenario for the Eurozone economy? And do we foresee a recession for 2024?

Bert Lourenco, global head of rates research, Crédit Agricole CIB: Relative to other houses, we are somewhat more optimistic, and even within CACIB, I’m probably more optimistic than my colleagues. We don’t expect a recession this year. In fact, we expect growth to pick up — still sub-trend, but just below 1%. What are the reasons for this?

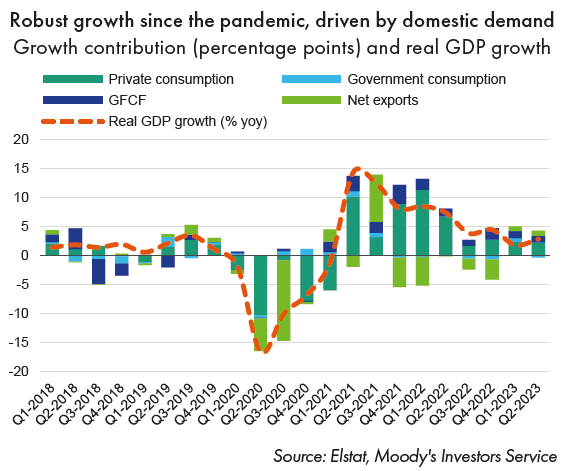

First and foremost, we had a terms of trade shock for the past few years, led by the energy crisis, and that’s clearly unwound itself. This is leading to the current account changing from a deficit to a surplus for the EU in general. Secondly, we still have pretty strong labour markets — which is pretty astounding — and these labour markets are still generating wage gains of 4.5% or so, so we think that real household incomes will increase, giving household consumption a boost. And then we have this phenomenon that is pertinent around the world, not just for Europe, which is that we have deficits, and these deficits seem to be structurally persistent. So in aggregate, governments have less net issuance this year, but when you throw in the EU and supranational issuance, that actually becomes a net positive, so we also have support through the fiscal side. When you bring all this together, that’s quite a good combination for a broadening out of growth.

One final thing to mention is the juncture of banks with the real estate sector. High interest rates have not caused as much pain in residential real estate as one might expect. There are pockets in the EU, like Sweden and Germany, that still have some pain to come in real estate. But overall, banks seem to be in pretty good shape, able to provide credit if there’s demand, which is pretty amazing given the level of rates we have right now.

So it’s really a matter of subdued, but better growth across Europe — but remembering that Germany is going to remain the sick man of Europe for a while, and so we should not depend on the German manufacturing sector to lead growth in Europe for some time at least.

Benyaya: In terms of the financial institutions primary market, what have we seen in the first two months of 2024? And how does it compare with early 2023?

Vincent Hoarau, head of FIG syndicate, Crédit Agricole CIB: Since the beginning of the year, the primary market activity in euro-denominated format has been very robust, around €140bn. Nonetheless, down 18% year-to-date versus 2023. Last year’s volumes were exceptionality high; 2024 volumes are still up 35% versus 2022, and twice the volumes of 2021. So far this year we have enjoyed issuance activity in line with what should be a reasonable pace in a normalised world post a decade of QE.

If we look at issuance in US dollars, it is exceptionally high, with numerous jumbo offerings from Yankee banks. This time last year, funding in US dollars was less competitive in terms of arbitrage for European banks; nonetheless, Yankee issuance is down 10% this year versus last.

Elsewhere, European issuers also continue to be active in sterling and niche currencies, looking to further diversify their funding sources. Lastly, on ESG, issuance is down 30%, but still up versus 2022.

In terms of demand and investor reception, the tone is particularly supportive and all the metrics we look at around deal execution have been great. Oversubscription levels are exceptionally elevated. The stickiness of demand when we adjust pricing lower in bookbuilding, the granularity and the quality of order books are great. Secondary performance post pricing can be impressive. New issue concessions have been drifting tighter since the beginning of the year, and are sometimes non-existent or even negative.

All those things point to a very healthy market. Investors love the current level of yields. The iTraxx financials is currently at a two year low.

Looking at the profile of issuance, in senior unsecured, tenors are well spread across the maturity spectrum. In covered bonds, 50% of supply has come with a maturity between five and seven years. Last year the average duration for funding was shorter than five years. The growing appetite for long dated assets is remarkable. We have seen much more 10-12 year new issues this year compared to last.

We see the most noticeable change across funding instruments in the covered bond space. 2023 was a record year in terms of issuance, but a very challenging one for covered bonds, a year during which the asset class digested the legacy of a decade of quantitative easing. The market has been dealing with ongoing technical distortions because of the lack of relevance of secondary market spread levels, which were kept artificially tight sometimes because of the purchases of the Eurosystem. After a year of repricing across jurisdictions, we started 2024 with much healthier trading metrics. Globally, the product has become much more appealing, while the buyer base has grown steadily. That’s a relevant evolution for FIs.

Benyaya: You mentioned that spreads are tight — why is that in the current environment?

Hoarau: A couple of elements explain the current spread complex. First of all, the demand side of the equation is supported by a very robust economy in the US, while the situation in Europe is improving significantly, particularly in the South and to some extent in France, even if we have the aforementioned situation in Germany. We also have a very favourable credit environment in spite of the string of rate hikes over the past two years. We have not seen a lot of credit events — yes, we had Credit Suisse and the US regional bank issues last year, but away from that the market has been extremely resilient. Over the past 12 months, we have enjoyed a very nice situation in terms of ratings evolution, with a lot of upgrades and many financial instruments moving from non-investment grade to investment grade. So that’s the first element.

The second element explaining why the spread complex situation looks really exceptional, is that the equity rally is also pushing pension funds to rebalance cash to the benefit of the credit market. And if you screen the world of investment grade credit funds, we continue to see tremendous inflows.

But most importantly, the yield environment combined with the excess liquidity situation is certainly what is keeping spreads so tight nowadays. And as long as the liquidity situation does not change, we are going to see a market that remains extremely resilient, and any sign of correction will very likely be short-lived. In this very particular rate environment, there is little upside in selling bonds, particularly high coupon bonds. And the recent negative headlines around commercial real estate for the time being remain isolated cases that are not derailing the market from its very strong path.

Benyaya: When it comes to the spread complex for Eurozone government bonds, and also ECB monetary policy, what can we expect?

Lourenco: At the start of the year, many people were looking for the ECB to start cutting rates even as early as Q1 of this year, which we thought was way, way premature. Our view is for three rate cuts in Q4, i.e. after June, and three rate cuts in the first half of next year. We think the ECB needs a lot more evidence to be fully comfortable that inflation is coming back to target, and that their fear of a policy mistake still points towards moving more slowly in cutting rates. And nobody’s going to be in a hurry to cut in large amounts — unless we have a recession, a hard landing — therefore, we foresee 25bp increments. The market still has a bit more than that priced in. So if you ask me what our view is on the rates side, we still think that yields can go up a little further, simply because we think the market’s got a little bit ahead of itself — you have a 25bp cut effectively priced in for June already, which we think is too early. And remember that they will come out with their forecasts in March, June and September. So really we think that more time is needed, and that the forecast in September will allow them to proceed with that cut.

Coming back to the first question, on the spread complex. What could lead to massive spread widening in EGBs? It could result from redenomination risk, but that doesn’t seem to be credible from a political angle for any country right now. It could possibly come from a big deleveraging event that sharply increases unemployment. Or counter-cyclical factors that result in a sudden deterioration in government finances. But these factors aren’t at play.

Our view — which is a little different than a year and a half ago — is that in spite of hikes, and in spite of QT, we have not been worried about spread widening. Why? Number one is that we have high nominal GDP. This is the impact of inflation. So government tax receipts are very good everywhere. That will be a supportive factor. Number two, high yields create demand. We’ve seen a transition away from institutional investors more to retail investors being interested in fixed income — just look at all the retail products coming out of Italy, Portugal, and now places like Belgium. So higher yields are not an impediment to keeping spreads tighter — we do still think that significantly higher yields leads to a bit of spread widening pressure, but nothing dramatic. So we don’t have the ingredients for the massive spread widening that people were so afraid of at the start of the cycle. If I’d asked a year and a half ago if you believed that spreads would be at these levels with the ECB having hiked rates 400bp and unwinding its balance sheet, you’d have said, no way. But that’s exactly what’s happened, and that’s actually a pretty good thing. I think the ECB has done a pretty good job along the way, which is a slow, well-flagged pace of QT, and at the same time creating the the perception, at least, that there are mechanisms in the background such that if dramatic spread widening happens, it can step in at any point in time. All these factors probably point towards any spread widening remaining modest. Lastly, I would mention that the general abundance of liquidity and performance of credit, with a lack of defaults, also supports this view.

Benyaya: How are expectations regarding ECB monetary policy affecting investor sentiment and investor positioning?

Hoarau: The paradigm has changed completely in 2024 versus 2023: at the beginning of last year, we had the end of the tightening cycle ahead of us; in 2024, we have the start of the easing cycle ahead of us. So while the management of monetary policy risk was on everyone’s agenda in 2023, it has been losing a lot of its relevance. Investors now feel much more relaxed towards any type of risks. They like the yield, and while they may dislike the spread, they just enjoy the carry, disregarding the timing of the first rate cut. I can imagine that at some point one or the other may lose patience. But for the time being, I would say, so far, so good. And we are in a situation, a very unique situation, where the relationship between rates and credit is inverted.

Benyaya: Staying with interest rates, but looking at it from a slightly different angle, banking ALM: we’ve seen the higher interest rates boosting net interest margins in some countries — not everywhere, but in some places — what could be the hedging strategies to maintain this type of net interest margin?

Yves Glaser, head of financial institutions advisory, EMEA, Crédit Agricole CIB: Indeed, in the southern part of Europe — Greece, Spain, Italy, Portugal — banks generally grant variable rate mortgages, although there is a recent trend towards a higher proportion of fixed rate loans. In the northern part of the euro area — France, the Netherlands, Belgium — banks tend to lend at fixed rates. In France, for example, typically more than 90% of production is fixed rate and for very long periods, 20 to 25 years. ALM likes a natural match between assets and liabilities. That’s a factor contributing to a shorter model on the liability side for banks in Italy and Greece. Overall, the duration of balance sheets in southern Europe is lower than in northern Europe, which makes net interest income more sensitive to a change in interest rates. Given the rise in market interest rates, the development of NII for retail activities in these countries has been very favourable.

As rates fall, banks with low balance sheet duration will lose this benefit relatively quickly and return to lower levels of NII. The question for ALM teams now is: is this a good time to increase balance sheet duration and lock in the benefit of current interest rate levels?

One welcome development is that the beta on deposits has been relatively low over this period. It has been a good stress test: we have had almost a 400bp rise in rates and overall, while there has been some decline and some outflows on demand deposits, it has been relatively limited. Customers have been much less reactive on their deposits in this rising rate environment than they have been on their mortgages to prepay when rates went down. This would argue in favour of increasing the duration of deposits.

Once you increase the duration of deposits, how do you increase the duration of assets to effectively get more stickiness in your net interest income? The first way would be to do a receiver swap. But historically, banks with a high proportion of floating rate loans have tended to use their liquidity portfolios to increase the duration of their assets, and not so much receiver swaps. So a natural way to extend the duration of assets and immunise NII against lower rates would be to buy forward bonds, thereby locking in the reinvestment rate of maturing bonds. In addition, buying forward bonds rather than doing a receiver swap will benefit from the fact that the EGB curve is steeper than the swap curve. Finally, hedge accounting of forward bonds is easier than for a swap because the forward bond is an all-in-one hedge, the hedge item is the bond that you will receive, whereas for a swap, a commercial item would be designated as the hedged item, with potential inefficiencies arising from basis risk or behavioural risk.

Finally, some banks are also looking to buy floors to protect their NII against lower interest rates. In the same spirit as buying forward bonds, buying a call on government bonds can be an efficient alternative to a floor, both financially given the shape of the curve, and operationally for hedge accounting. Also, in terms of P&L profile, buying a call may be more suitable as the time value would be recorded in the initial period when NII is at a high level, whereas for a floor this time value would go to the P&L over the entire maturity of the hedge.

Benyaya: In terms of banking supervision, I know that there is a 200bp stress test set out in the regulation, but you mentioned we have experienced well above that. Do you have a view on how this could develop?

Glaser: The regulatory stress of 200bp was supposed to be the 99th percentile of interest rate stress, so once in 100 years, and we have had a 400bp move in interest rates. A revision of the stress level is currently within the scope of the regulator. In addition, we have had in the last two years bank failures as a result of interest rate risk, in particular SVB. This is another incentive to review the regulation. Pablo Hernández de Cos, chairman of the Basel Committee, gave a speech on the subject in September last year and raised the issue of IRRBB being in Pillar 2. However, moving IRRBB to Pillar 1 would be a very long shot. In addition, at the end of that speech, he also mentioned that these failures were more related to poor risk monitoring by these institutions than a structural problem for the banking sector which is related to Pillar 2.

In any case, we could see some changes in regulation, and in particular in the level of interest rate stress. Currently, there are discussions about extending the stress from 200bp to 250bp, which could be significant for some retail banks that manage their interest rate exposure close to the limit. Supervision is also likely to focus more on the IRRBB models used by banks, especially on deposit outflows, as large deposit outflows were the trigger for the SVB failure.

Benyaya: Let’s turn to sovereign ratings, where we have seen some divergence among countries. What is your view on such rating developments, also with reference to the Greek sovereign?

Lourenco: As a general observation, credit ratings don’t really give investors much of an advantage, because rating agencies are very much backward-looking. That doesn’t mean that they’re not important, simply because ratings are used by investors to invest in other domiciles, by risk management committees, and even for investors, they provide a kind of anchoring for valuations. They are also used by CCPs, for example, and as such give a kind of indication of what the value of such collateral might be. That’s a roundabout way of saying that you cannot ignore them.

Having said that, there are many metrics rating agencies look at, but crucial is if you’re running surpluses or deficits on the fiscal side, and likewise for the current account. There are a few countries in Europe that have these twin surpluses, while a few have twin deficits. Those with twin surpluses are Greece, Portugal and Ireland, and these are the smaller countries that have positive ratings momentum. We think that they’ll still be subject to upgrades in the future, as long as we don’t get a massive recession and there’s no big deleveraging event. Meanwhile, the bigger countries with twin deficits are those we are a little more worried about, such as Belgium and France. We’re not so concerned about Italy or Spain for the time being. That’s how we differentiate among European sovereigns. So we would still be positive on Greek developments given what’s happening here at a fundamental level.

(See ratings focus below for more on Greek upgrades.)

Benyaya: On the back of this positive momentum in Greek sovereign ratings, how is Greek risk perceived in the credit markets?

Hoarau: People are chasing Greek assets. The rating trajectory of the country has been decisive in spread developments for the country. Investors are really impressed by the pace of the reforms, and how austerity has paid off in recent years. It’s not about cleaning balance sheets now; good banks are again on the offensive. And we could have further good news from Moody’s this year on the sovereign, with the ratings of Eurobank and NBG benefiting. In any case, the trajectory of Greek metrics are clearly reflected in the evolution of spreads in the secondary market: over the past 12 months, Greek senior bonds have tightened by an average of something like 200bp. When I’m looking at headlines nowadays, with what’s happening in Germany compared to what’s happening in southern Europe, it’s quite a turnaround.

Benyaya: Before we open the Q&A to the audience, one final question to each of our panellists on risk factors for the rest of 2024. Yves, as alluded to earlier, clearly interest rate movements can result in some arbitrage strategies by clients and depositors. How is this risk factor reflected in banks’ interest rate risk management, and do you see any potential changes in the course of the year?

Glaser: During the decade of very low interest rates, we have seen a surge in sight deposits in almost all countries. I like to look at the ratio of sight deposits to household disposable income. For a long time this was very stable — from the late 1990s to around 2010 — but from 2012, when interest rates were zero or negative, the ratio started to rise and by 2020 it was more than double what it was at the end of 2010. So we clearly have a lot more demand deposits now relative to household disposable income. And so far we have seen relatively low deposit outflows. This situation may not last, as there is no reason why customers should be less efficient today than they were 20 years ago. It takes time for customers to regain a deposit culture. Deposit outflows may also continue if interest rates remain at current levels. On the other hand, if interest rates return to lower levels, we may see an increase in prepayments on recently sold fixed rate mortgages. So there is certainly quite a significant behavioural risk on balance sheets. The supervisory teams are looking at this very closely, reviewing banks’ IRRBB models and requiring them to incorporate hypotheses about arbitrage from non-interest-bearing to interest-bearing products.

Banks have developed models that link the stability of deposits and the level of prepayments to the level of interest rates, which is a good response to this uncertainty. They are trying to hedge this exposure to behavioural risk. We see this in the demand for options products.

Benyaya: Bert, not another question on interest rates, but one on inflation. I believe inflation forecasts have been relatively sticky. What are the risks to these forecasts given that inflation seems to be easing somewhat?

Lourenco: First of all, I’d note that one of the things that makes us a little bit different from other research shops is how much time and effort we spend analysing the inflation side. With the ECB having a strict and, I should stress, symmetrical inflation target, inflation developments are uppermost in our mind in terms of how we think about the market.

For this year, we expect the decline in inflation to proceed, but it might not proceed as fast as the market has priced in. We think it’ll be a little bit higher than implied, particularly in the CPI fixings for the second half of the year. At the start of the year, we thought inflation would probably come in at 2.5%-2.8%, although following some better developments recently, we’re probably talking about around 2.5% HICP on average for the year. Two factors explain this higher inflation. One is tight labour markets, and wages, which imply that service wages stay high — as I mentioned earlier, we have wages growing at around 4.5%, so core inflation will by default stay high. And then the other thing that we consider a lot is food price inflation, simply because of what’s happening with the climate, the cost of food production — just look at the farmers’ protests across Europe. These two factors to us imply that inflation will probably be a bit higher than others expect.

The last point I would make is that a lot of people are looking at inflation dynamics returning back to what they were before Covid, and we’re not so sure about that. It could be that we have sufficient changes in structural factors, be that industrial policy, changing global trade patterns, particularly Asia and China, potentially the implications of green energy investment, more military spending and so on, and continued pro-cyclical fiscal spending. These kinds of structural factors imply that, this time around, we don’t expect inflation to be below 2%, we think that it will stay somewhere around 2% going forward. It still means that the ECB can cut rates, but it means that we’re not going back to a low inflation environment like we had in the past, and probably not a very low rate environment, either.

Benyaya: Vincent, what risk factors do you foresee for the FI primary markets for the rest of 2024?

Hoarau: I’m fairly bullish, I have to say, at least for the first half of the year. If I have to list some potential risk factors, I would start with a theoretical one, which is the increase of Minimum Reserve Requirements by the ECB. This could push up supply and increase potential pressure on spreads, but I think this risk is only theoretical as long as the liquidity situation remains intact. More important, and later in the year, could be refinancing risk driven by booming SSA supply and the refinancing of ballooning budget deficits. And clearly reflation risk would be a disaster for markets. This is certainly improbable, but if we have no rate cuts this year, and a narrative grows up around rate hikes instead of rate cuts, it could derail the market from this very strong base, and this is something we are all bearing in mind.

Benyaya: Thank you all for your insights. So now I’m happy to open the Q&A session.

Audience member: Going back to the regulatory environment, if I’m not mistaken, there’s a focus on the credit spread risk for the banking book, something that might become mandatory or at least that the regulator is monitoring. How do you see the banks in Europe working on that? And what’s your view on the final outcome?

Glaser: That’s a tricky question because I don’t think there’s a consensus on how to track credit spread risk in the banking book. It’s a new requirement from the EBA to have a risk framework for CSRRBB and there is a lot of reluctance on the part of banks to have a generalisation to the entire banking book. There are heterogeneous practices but I think that many banks have a restrictive view on the scope of CSRBB, which is mainly limited to their bond portfolio and does not include the loan book. On the liability side, I don’t think banks include their funding spread in the scope of CSRBB. Having their own credit spread in the scope of CSRBB would mitigate the stress on the asset side. The ECB would probably be reluctant to have this attenuation factor in case of a widening of the credit spread. So far, it is probably mainly been an appreciation of the bond portfolio’s exposure to credit spread widening.

Audience member: You haven’t discussed the possibility of Trump being elected, or all the other elections taking place this year. What are your thoughts on this front?

Hoarau: That could be a factor in why I’m more bullish on the first half of the year rather than the second half… When it comes to the direction of spreads and risks for markets, it’s primarily a question of liquidity and market absorption capacity. Then we look at geopolitics and that element can go with the liquidity dynamic and refinancing risk if the question around European defence funding comes up. In the US, the fiscal lever will be heavily used either way. But one scenario potentially implies more pressure on the issuance front in Europe, and potentially on the spread complex in the lower beta part of the borrower spectrum (government and supra).

Lourenco: The way I look at it is that for markets, what matters is the politicians’ positions on deficits, and be it Trump or be it Biden, the reality is that neither seems committed to bringing down the deficit substantially. Large deficits by definition imply high nominal GDP, and if you have high nominal GDP, that’s by definition good for risky assets and for markets in general. So we shouldn’t overplay the impact of the difference between the two, as it’s not that big in terms of what it means for the fiscal equation. As for one being more pro-business or against it, the perception is probably that Trump’s more pro-business. What that implies for global trade, sanctions and so on, that’s a different question.

Audience member: How would you assess the second round effects of the increase in wages for inflation?

Lourenco: If wages keep increasing, service inflation will stay high. And household real incomes should get a progressive boost, which is actually good for the growth equation. Quantifying this is quite difficult, but if we continue to see wages above 4%, continuously, that just means that other factors within the inflation mix will have to come down. So it just delays the easing cycle. Does it imply that we get hikes? I’m not so convinced that’s going to be the case. If we had high wages for a long period of time and a supply shock — with oil prices increasing dramatically, for example — that would really change the market’s perception of what the ECB will be doing.

Bank upgrades eyed in wake of sovereign’s

After more than a decade in sub-investment grade territory, Greece was in the autumn rewarded for reform efforts by receiving a series of upgrades that saw it finally regain investment ratings, with only Moody’s yet to take this final step.

S&P was the first of the “big three” rating agencies to upgrade the sovereign back into investment grade territory, lifting it from BB+ to BBB- on 20 October 2023.

Implementing a stable outlook, the rating agency cited an improvement in public finances thanks to budgetary consolidation efforts, noting that since the debt crisis of 2009-2015, significant progress has been made in addressing the country’s economic and fiscal imbalances.

“We expect additional structural economic and budgetary reforms, coupled with large EU funds, will support robust economic growth in 2023-2026 and underpin continued reduction in government debt,” said S&P.

Fitch followed suit on 1 December, also lifting Greece from BB+ to BBB-, on stable outlook. High among key rating drivers cited by the rating agency were favourable debt dynamics.

It noted that a projected decline in the debt to GDP ratio of 65pp, from a pandemic high of 205% to a forecast 141.2% in 2027 would be among the best performances of any Fitch-rated sovereign. The rating agency acknowledged that the ratio is forecast to remain close to three times the BBB median, but said mitigating factors such as low debt servicing costs, very long maturities (18 years) and a substantial liquid cash buffer (around 16.5% of GDP mid-November) reduce public finance risks.

A commitment to fiscal consolidation was the other factor uppermost among drivers of Fitch’s upgrade. The primary surplus was set to increase to 1.1% of GDP and average 2.2% in 2024-2025, according to the rating agency’s forecasts.

“Fiscal prudence is anchored in conservative expenditure assumptions in recent budgets (and is also the case in the 2024 budget),” said Fitch, “with revenue over-performance providing fiscal space for temporary spending: in 2023 this included energy crisis and climate change-related measures.”

With Scope Ratings having upgraded the Greek sovereign from BB+ to BBB- in August 2023 and Morningstar DRBS having lifted it from BB (high) to BBB (low) in September, the next move from Moody’s is awaited. A Moody’s upgrade in September left Greece on the cusp of investment grade, at Ba1, on stable outlook, although the rating action was by two notches, from Ba3. The rating agency cited several factors that could lead to an upgrade.

“A continuation of economic policies and commitment to fiscal consolidation, together with successful implementation of remaining reforms, particularly in the judicial system, leading to greater resilience to external shocks, faster than expected improvement to fiscal strength and work-out of non-performing loans (NPLs) would support a higher rating,” said Moody’s. “In addition, a more rapid change in Greece’s economic structure that helps to improve economic resilience would be credit positive.

“Further improvements in the banking sector,” it added, “reducing volatility of profitability and bringing asset quality and capitalisation ratios closer to the euro area average, would also be credit positive.”

Moody’s two notch upgrade of the sovereign was accompanied by an improvement in its macro profile for Greece from Moderate- to Moderate+.

This contributed to the six Greek banks rated by Moody’s benefiting from one or two notch upgrades in the wake of the sovereign’s, with all on positive outlook.