CEE GDP advances stymied as Iran war ramps up inflation pressure, conflict duration key

How long it takes for Trump to find an off-ramp from the Iran conflict is set to determine the extent of economic fallout from the conflict, according to Crédit Agricole CIB and Erste Group analysts, with CEE countries braced for a temporary setback to their upward trajectories.

Valentin Marinov, Head of G10 FX and UK Research, Crédit Agricole CIB, noted that despite dipping sharply upon the outbreak of the Iran war, investor appetite for risk assets has proven more resilient than episodes such as Liberation Day last year, not to mention Russia’s invasion of Ukraine in 2020 — despite oil and gas prices having rallied very aggressively and pricing in an extended impact.

“Why is it that against that backdrop risk sentiment is so resilient?” he said. “The answer is TACO — Trump always chickens out. Everyone can smell the TACO, everyone is hoping that one day President Donald J Trump will wake up and say, you know what? I’ve had enough.

“And every day, people are coming back to me saying, you know what? Maybe risk is a buy. Maybe the war in Iran is coming to an end.”

However, Marinov (pictured) cautioned that while the market apparently wants the conflict to be over as soon as possible, and took heart from the ceasefire announcement, a resolution won’t be straightforward. Observers have noted that while Trump could unilaterally walk back tariffs, an end to the Middle Eastern conflict will depend on Iran, potentially Israel and other factors beyond his control, as highlighted by developments since negotiations started in Islamabad.

“My sense is that, well, it’s not over until it’s over,” said Marinov. “The key challenge now for everyone is timing the end of this conflict.”

According to the International Energy Association, oil reserves stood at 1.6bn barrels before the conflict, 400m have already been released to compensate for the loss of around 20m barrels of oil due to the blockage of the Strait of Hormuz, and the remainder could be gone in around two months.

“The bad news for Europe,” said Marinov, “is that most of those reserves are elsewhere — they are either in the US or Japan — meaning that I would give it until the end of May, before the pain starts to become really palpable. By that, I mean governments — here or in central and eastern Europe — asking their citizens to work remotely, travel less, and ultimately try to curb energy consumption.

“And I would hope that at that point, the pain for US consumers, the pain for President Trump, will become significantly less bearable than it is now. This is my personal guess on timing.”

The Iran war is in any case a “considerable negative energy supply shock” that Marinov said will stymie Europe’s recovery, reignite inflation, and impact central bank actions.

A worst case scenario of persistently elevated oil and gas prices — with, for example, European gas prices hitting and remaining at the highs of the Ukraine war — could see Eurozone core CPI inflation rise above 4% and GDP growth flat this year and slightly negative in 2027. That scenario was the fifth of five modelled by Crédit Agricole CIB, with more moderate scenarios — the second and third — seeing inflation remaining contained and growth closer to 1%.

A recession in Europe should be avoided, said Marinov.

“We doubt that we’re going to see a replay of the onset of the Ukraine war in 2022 that triggered an energy crisis and threatened to lead to a fiscal crisis in Europe,” he added. “It is a risk, but we doubt that this will be the outcome.

“We do believe that in central and eastern Europe, the resilience of domestic demand and the continuing positive spillover effects from the aggressive fiscal stimulus programme in Germany should prop up the economies and indeed their currencies.”

Alen Kovač, Chief Economist, Head of SEE Macro and Fixed Income Research, Erste Group, agreed such factors should be supportive of CEE economies, but noted that the Iran war nevertheless meant that 2026 would not live up to pre-conflict expectations, which had been for an improvement on a somewhat disappointing 2025.

“We are now in a situation where this optimism — which had been supported PMIs, for example, as well as the economic sentiment index — has started to slowly deteriorate, especially looking at consumer confidence on the CEE average level,” he said, “and clearly the outlook has been burdened by the inflation narrative, with inflation more or less killing the disposable income gains that had been anticipated in the CEE landscape this year.”

An average CPI impact of roughly 0.6%-0.7% in the region will pressure real wage growth, which had already been easing, noted Kovač, with labour markets also showing some cracks as unemployment comes off record low levels.

On the investment side, billions of euros of funds available to CEE countries in 2026 from EU programmes should provide a significant buffer, supporting growth and mitigating external headwinds, according to Erste. SAFE (Security Action for Europe) funds are coming on stream alongside the MFF and RRF funds already being used.

Kovač (pictured) meanwhile highlighted the diversity in performance of different CEE countries, which is sometimes overlooked.

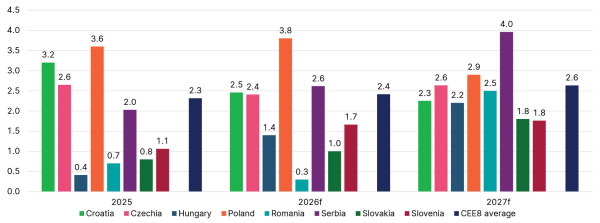

“Especially in the last couple of years, we definitely do see the CEE space like an environment of multi-tier growth lanes,” he said, “in the sense of, economies that are doing really well in terms of growth — predominantly Croatia and Poland — then economies that are somewhere in the middle — like Slovenia, Czechia — and finally economies that have been struggling — Hungary, Romania, and lately Slovakia.

“We see growth in 2026 remaining quite diverse in the region,” added Kovač, “with Poland being the top performer, and Croatia and Czechia holding a rather solid level.”

Hungary and Romania have been hit hardest in terms of revisions to 2026 GDP expectations, with the latter the weakest performer in the region, especially given how fiscal consolidation is impacting its economy.

“At the CEE level,” said Kovač, “we now see growth very similar to the 2025 level, with risks to the downside. This would be something like the second scenario of Valentin. Hopefully, we are not going into the additional levels of stress — going towards the more adverse scenario, we would see an additional shock of roughly 0.5%, depending on the country.

“But our baseline is that, compared to previous levels, the growth profile remains relatively resilient in the region.”

Erste expects Hungary and Romania to avoid negative rating actions this year, while Kovač noted that Croatia enjoyed a one-notch upgrade from S&P last month, from A- to A.

CEE8 average growth now expected at 2.4%, down 0.3pp — Forecast revision reflecting geopolitical realities

Source: Erste Group Research

Longer term, CEE countries could be the beneficiary of pre-Iran conflict trends reasserting themselves more firmly, according to Marinov.

“Global investors were in recent years overinvested in the US, especially with the AI craze starting, with people really wanting a piece of the action acquiring US assets, dollar assets, offering superior returns with superior liquidity,” he said. “Then President Trump came along, and the first cracks in the idea of US exceptionalism and that US trade started to appear, and those cracks are likely to deepen.

“The war in Iran is likely to make it more difficult for investors to justify an over-exposure to the US, and as a result, there’ll be growing demand for diversification out of the US and into somewhere else.”

Central and eastern Europe could be where they turn to, said Marinov.

“Why? Because of better returns. Essentially, CEE is like everything that’s good about investing in Europe, but with extra carry on top.

“Ultimately, as an investor, you are looking at the risk-reward ratio more than anything else,” he added, “and while you may not be getting the very best carry out there, we believe that in terms of risk-reward, there are opportunities in central and eastern Europe far superior to what you can get elsewhere.”

You can download a pdf version of this article and related coverage here.